The Ultimate Guide to setting your Ideal Cash Flow Profile

We have written a number of blogs with the intention of helping you understand your cash flow picture, so you can take control of your business…..before someone else does.

If you have been reading our blogs and practiced the use of our tools and processes, you will have a clear understanding of each component that make up your cash flow picture. You will also be able to see the full cash flow picture of your business, clearly. This will serve as your inspiration to make changes towards improving your cash flow position.

But we realise that people still do not know how to fix their cash flow problem, or even make changes for the better. You wish to improve, and you hope to improve, but, somehow, you end up in the same position as before, year after year.

So it is our desire to equip you with the knowledge, the processes and the tools to help you improve your cash flow – this is, to help you move your cash flow towards the desired position.

We want to teach you how to improve your cash flow position. We will be looking at the process you need to follow to fix your cash flow problems. Here are the steps you need to take:

- Set your ideal cash flow profile

- Set the performance criteria

- Roll the programme out across the whole business

In this blog, we will look closely into Step 1 – Setting your ideal cash flow profile. We will give you a Framework you can use to set your ideal cash flow profile to maximise your success!

Having a clear definition of your cash flow profile is one of the most important thing you could do for your business. Your ideal cash flow profile dictates everything, from your price, volume, overheads to when you pay your suppliers, hold stock/WIP (Work In Progress) or when your customers pay you.

You choose all of these elements, so it is not limiting….it is so EMPOWERING!

There are a number of ways for you to come up with your ideal cash flow profile, but over time we have developed a framework that works really well for our clients. And we continue to evolve it…

Universal Cash Flow Profile

Sorry…..there is no universal cash flow profile….your cash flow profile is a moving, dynamic thing that you will go back to and modify – often.

Ultimately, you should think of your ideal cash flow profile as resources you will need to dedicate – Finance, Marketing, Operations etc. in order to generate more cash flow.

In fact, your ideal cash flow profile is specific to:

- Your business model

- Your goals

- Your capabilities

But, before you can develop your ideal cash flow profile you must overcome….

The Fear of Missing Out

A lot of leaders we work with fear narrowing things down or making changes, even though they are clear on the benefits of doing so. They fear of losing customers or missing out on prospective deals or some other fear….and that is due to a FEAR OF MISSING OUT. They think if they make changes, they will upset particular groups or ‘hurt’ their business.

But the reality is that when you do not focus, and you try to please everybody, when you do not improve matters, the only person missing out is you and your business. You are missing out on every one of those opportunities to generate more cash in your business; you are missing out on attaining your ideal cash flow position.

So to overcome your fear….

SITUATIONAL Awareness is critical

Determining your ideal cash flow is NOT about determining cash flow for ONLY one client segment or one product line. It is about determining the ideal cash flow for a particular situation, or situations. This situation could be determined by one or more elements or Financial Levers.

That should ease the pain a bit.

The situation definition has three inputs:

1. The timeframe Input

90 days is a good time frame for testing: less than that is not enough time and more than that could be beneficial only in particular cases. The key is to be specific with the overall timeframe and to identify milestones to check if this time frame is suitable and sufficient.

2. Your Goal

Be specific with the goal you wish to achieve in the timeframe.

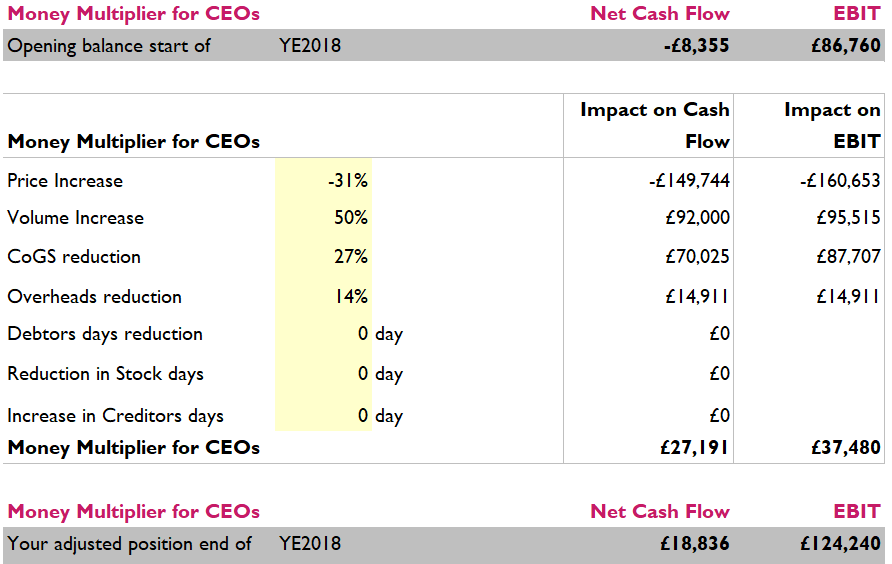

- Price increase (percentage)

- Volume increase (percentage)

- Direct costs reduction (percentage)

- Overheads reduction (percentage)

- debtors days reduction

- creditors days increase

- stock/WIP days reduction

Use our Money Multiplier for CEOs to figure out your goals, based on how changes in any of the above drivers will impact your cash flow and your net profit.

> Get my Money Multiplier for CEOs now! <

You should be clear that once you define the time frame and the goal (which could be one or a combination of the above elements), your ideal cash flow becomes very, very important. Reaching that specific goal in the specific time frame without being extremely deliberate in your cash flow generation efforts is essentially a non-starter.

You will also need to be clear on where you are starting from (baseline) and what metrics you will use to measure your progress for this situation (and ensure you are keeping track of those).

3. Your current capabilities

This final point is critical; regardless of what your goals are, you have to be realistic of what your capabilities are and what you are able to do. Sometimes your staff might have a skill that is outside of your core capability, which could be used to create specific outcome towards your goal. But you need to be realistic about their individual workload and how much stretch they can handle.

Objective and Pragmatic Method

The Ideal Cash flow profile Framework is a practical method that allows scientific approach to your cash. It is the only way that allows you to test your BUSINESS MODEL.

If you have 90 days to acquire 90K and you are not at 30K at the end of 30 days you can decide to change your tactics, keep going, or pivot to a new ideal Cash flow profile – if you feel the profile you came up with isn’t working for you or it was just wrong.

It’s so much better to know something is not working and be able to make changes, than to just keep ending up in the same place, over and over again….and this method gives you more pragmatic and less subjective method to achieve that.

OK, so we are moving now onto the actual framework, but MAKE SURE you read the Situational Definition…it’s ABSOLUTELY CRITICAL. Without clearly defined situation, just defining an ideal cash flow will NOT work.

A NOTE about use of the Ideal Cash Flow Framework in GROWING Firms

When developing an Ideal Cash Flow Framework from scratch for the purpose of generating more cash and profit, you will start with a goal and the time frame; for example, reduce the debtors’ days by 20 days in 90 days.

So for you to reach that goal in that timeframe, you need to identify what changes would contribute most to achieving this goal within the timeframe. Then turn these changes into a formal KPI structure against which you could measure how your cash flow is progressing.

OK, so here is YOUR…..

Ideal Cash Flow Profile Framework

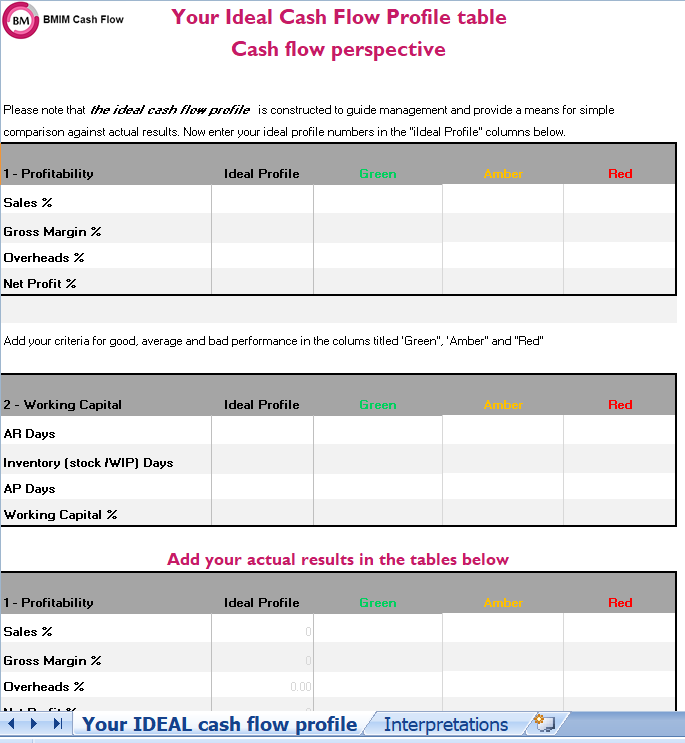

The purpose of the ideal profile is to guide you and your team and enable you to compare against actual results.

Below is the breakdown of the Framework, starting with the baseline components:

1. Profit

When we talk about profit, in the context of Ideal Cash flow profile we mean the DESIRED PERCENTAGE of the following four elements or Financial Levers:

- Sales – your revenue should be 100%. You want to achieve this number, ideally. But we know in reality unexpected things happen, such as drop in price or loss of customers and you end up with less revenue. That is why you will have to construct a monthly results table, to demonstrate how you are doing in light of the KPI set. More on this topic in a different blog.

- Gross Margin – this varies based on your business model, your industry etc. As you know you should aim to increase this percentage over time.

- Overheads – your business has direct control over your overheads, and again, you should aim for lower percentage.

- Net profit – a healthy business has over 15% net profit, but this varies based on the type of your business. A good start is 10%, as you should not drop below 10% and then aim to move up from here on. When you add more staff, this percentage will drop, but make sure it does not go below 10%.

2. Working Capital

Similarly, when we talk about working capital, in context of the Ideal Cash Flow profile, we mean the DESIRED number of DAYS of the following four elements or Financial Levers:

-

- Debtors (Accounts Receivable) – typically 30 days payment terms will give you average debtors days of 60 days and if you are good at collections 45 days is a really good performance.

- Inventory (stock or WIP) – again, this depends on your business model. Just make sure you optimise your inventory to ensure you can service the market but also not to lock too much cash in it.

- Creditors (Accounts Payable) – this will depend on your relationship with your suppliers. The bigger, the better, so if you could aim to achieve 60 days, it is a good start.

- Working capital (percentage of sales) – how much working capital is ideal for your business depends on your sales revenue, your business model as well as your strategy e.g. if you are growing, or expanding. To work this number out you will need to analyse your working capital cycle, so you can predict the ideal working capital. Make sure to consider seasonal spikes in sales and use every opportunity you have to quickly convert each element in the cycle into cash (to avoid relying on external finances).

Ideal Cash Flow Profile defined; now What?

Download your Ideal Cash Flow Profile table and start constructing your monthly results. This is great guide for you and your team and it provides a means for simple comparison against your actual results.

> Show me my Ideal Cash Flow Profile table now! <

Take this further by adding three more columns to represent good, average and bad results, to show clearly how you are doing in light of your KPIs. More on this subject in our next blog – Setting your cash flow performance criteria.

I hope this helps you to take your cash flow to the next level!! Keep us posted with you progress, or just send us your comments and questions: info@bmim.co.uk